This report describes the 2013 taxes and

incentives provided by 28 countries around the

world to promote renewable energy from wind,

solar, biomass, geothermal and hydropower.

These policies also support other areas such

as increased energy efficiency, smart-grid

management, biofuels, carbon capture systems

and storage technologies. Content includes an

introduction about global trends in renewables,

a summary of investments in renewable

energy, and a brief outline of renewable energy

promotion policies in all 28 countries.

André Boekhoudt

Head of Global Energy

and Natural Resources

Tax Practice

Lars Behrendt

Tax Partner, KPMG in

Germany

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Contents

Introduction

1

2013 Industry trends

2

Global investment in renewable energy production

3

Renewable energy promotion policies by country

5

Argentina

7

Australia

8

Austria

10

Brazil

11

Canada

13

China

16

Denmark

18

France

20

Germany

22

India

24

Ireland

26

Italy

28

Japan

31

Mexico

32

The Netherlands

34

New Zealand

36

Norway

37

Peru

39

Poland

40

Romania

41

South Africa

43

South Korea

45

Spain

46

Sweden

49

Turkey

50

United Kingdom

51

United States

53

Uruguay

55

Top five countries 2012

57

Appendix A: REN21 2012 Renewables Global Status Report

58

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

1 | Taxes and incentives for renewable energy

Introduction

Renewable energy continues to be

one of the world’s strongest growth

industries. Consider these facts:

• Approximately20percentofglobal

electricity generation now comes from

renewable energy sources.

1

• Renewablesaccountedforover

half of total net additions to electric

generating capacity worldwide

in 2012.

2

• Almost70percentofnewelectric

generating capacity in the European

Union (EU) for 2012 came from

renewables.

3

• Solarphotovoltaic(PV)electricity

generation soared from 10 gigawatts

(GW) in 2007 to over 100 GW in 2012.

4

This rapid increase in renewables is

driven by a number of factors, including

falling technology costs, rising fossil-fuel

prices and carbon pricing. However,

the main support for growth is through

government incentives, which totaled

United States dollar (USD)88 billion

globally in 2011.

5

This report describes current incentives

provided by 28 countries around the

world to promote renewable energy

from wind, solar, biomass, geothermal

and hydropower. These incentives

also support related areas such as

increased energy efficiency, smart-grid

management, biofuels, carbon capture

systems and storage technologies.

Governments now offer a wide

variety of tax incentives and related

programs to support renewable energy

investment, including:

• credits

• grants

• taxholidays

• accelerateddepreciation

• non-taxincentives.

Governments also play a role in

discouraging carbon emissions by

enforcing taxes and penalties such as:

• carbontaxandpricing

• capandtradeschemes

• indirecttaxes,suchasenergy

taxes, excise taxes or value

addedtaxes(VATs).

The 12 most common policies can be

divided into three categories:

• Regulatorypolicies:

– renewable energy targets

– feed-in tariff/premium payment

– electric utility quota obligation/

renewable portfolio standard (RPS)

– net metering

– biofuels obligation/mandate

– heat obligation/mandate

– tradable renewable energy

credit (REC).

• Fiscalincentives:

– capital subsidy, grant and rebate

– investment and production tax

credits

– reductions in sales taxes, energy

taxes, CO

2

taxes,VATandother

taxes

– energy production payment.

• Publicnancing:

– public investment, loans and

grants

– public competitive bidding/

tendering.

These policies and incentives have

proven their effectiveness over the past

decade. By the end of 2012, at least

138 countries had renewable energy

targets, an increase of 66 percent from

2007.

6

Some 120 countries have various

types of policy targets for long-term

shares of renewable energy. The EU is

maintaining its target of 20 percent by

2020.

7

Several European countries in

particular have even stronger national

long-term targets that will place them in

the high renewables range by 2030 or

2050, including Denmark (100 percent)

and Germany (60 percent).

8

Outside of Europe, at least 20 other

countries have targets in the 2020–

2030 time frame ranging from 10 to

50 percent. These include Algeria,

China, Indonesia, Jamaica, Jordan,

Madagascar, Mali, Mauritius, Samoa,

Senegal, South Africa, Thailand, Turkey,

Ukraine,andVietnam.

9

(For additional information about these

policies, see appendix A/page 57).

1

World Energy Outlook 2012 – Executive Summary

2

Ibid.

3

REN 21 Renewables 2013 Global Status Report

4

Ibid.

5

Op. cit., World Energy Outlook 2012

6

Op. cit., REN 21 Renewables 2013 Global Status Report

7

REN 21 Renewables 2013 Global Futures Report

8

Ibid.

9

Ibid.

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Taxes and incentives for renewable energy | 2

2013 Industry trends

The global energy system based

on hydrocarbons is undergoing a

foundational shift. No one disputes the

need for increased energy supplies.

Global demand for electricity is

expected to rise by more than

80 percent from 2010 to 2040, driven

by an increase in total population and

gross domestic product (GDP) output.

To address world energy demand, the

energy industry has seen a recent

resurgence in oil and gas production,

led by the “shale gale” of natural gas

made available with hydraulic fracturing

(fracking) and horizontal drilling in

the US In addition, global fossil fuel

subsidies rose almost 30 percent to

USD523 billion in 2011, primarily for oil

development in the Middle East and

North Africa.

10

Nevertheless, the feasibility of a

carbon-based energy system is being

questioned. Economic development

across Europe is hampered by

continued high oil prices, and signs of

an unsustainable energy system persist,

with CO

2

emissions at a record high.

Accordingly, economies around the

world are increasing their dependence

on sustainable energy sources to

help reduce greenhouse gas (GHG)

emissions and pollutants. Renewables

have also been recognized as a way to

stimulate economies, enhance energy

security and diversify energy supply.

In terms of renewables policy, the EU

continues to lead the world in its support

for less carbon-intensive electricity

generation, with 65 percent of electricity

now being generated from nuclear and

renewable fuels. Europe increased its

wind energy capacity by 12.3 percent

in 2012,

11

and 20 percent of Europe’s

power is targeted to come from wind

generation by 2040. A European

Commission report indicated that

renewable energy could meet 55 to

75 percent of final energy consumption

by 2050, compared to less than

10 percent in 2010.

12

The United States is expected to see a

significant growth in domestic natural

gas production, which might impact

policies that support renewables.

Continued low gas prices, for example,

would likely reduce the value of

purchase price agreements available to

generators, including wind developers.

However, the federal Production Tax

Credit for wind was extended for a

further year by Congress at the start of

2013. The Clean Energy Standard Act of

2012 is currently under consideration

by the US Congress, and this law would

set the first nationwide targets for clean

electricity, defined as energy produced

from renewables, nuclear power and

gas-fired generation. The Renewable

Fuel Standard, adopted in 2005 and

extended in 2007, mandates 36 billion

gallons of biofuels to be blended into

transportation fuel by 2022.

In China, electric energy demand is

expected to more than double by

2040.

13

Despite the continued use of

large amounts of coal and gas, China is

also adopting the European and the US

approach to shift electricity generation

away from coal. China’s renewables

policy is based on the 2005 Renewable

Energy Law. In 2009, China set a target

to increase the share of non-fossil

energy (nuclear and renewables) in the

power sector to 15 percent by 2020.

The 12th Five- Year Plan (2011-2015) calls

for 70 GW of additional wind capacity,

120 GW of additional hydropower and 5

GW of additional solar capacity by 2015.

Targets have also been set for the first

time for geothermal and marine power.

Japan’s renewables energy policy

was reviewed and extended through

legislation passed in 2009 and a revised

Basic Energy Plan in 2010. After the

events at Fukushima, the government

announced the Innovative Strategy

for Energy and the Environment in

September 2012, which includes the

goal of reducing the role of nuclear

power. This will be supported in part by

increasing the deployment of renewable

energy. By 2030, the strategy calls for

power generation from renewables to

triple compared to 2010, reaching about

30 percent of total generation. In July

2012, Japan launched a new feed-in

tariffs system for wind and solar power

and other renewables, providing a

generous amount of incentives.

Overall, the global adoption rate of

renewables policies has slowed

considerably, especially as compared

to the early-to-mid 2000s. Revisions

to existing policies are becoming

increasingly more common, as well

as new types of policies that combine

energy-efficiency measures with the

implementation of renewable energy

technologies.

14

Looking ahead, recent analysis has

suggested that the following global

milestones will be reached by 2035:

15

• Demandforelectricitywillgrowby

over 70 percent.

• Overallenergydemandwillriseby

over 30 percent.

• Generationfromrenewableswill

increase to almost three times its

2010 level.

• Theshareofrenewablesinthe

generation mix will increase to

31 percent.

Greater energy efficiency in building,

heating, transportation and

manufacturing will help offset the rise in

energy demand. However, renewables

will play a vital role in addressing

this demand in an environmentally

supportive and sustainable manner.

10

Op. cit., World Energy Outlook 2012

11

EurObserv’ER, Wind Power Barometer

12

Rethinking 2050, European Renewable Energy Council, 2010

13

Op. cit., World Energy Outlook 2012

14

Op. cit., REN 21 Renewables 2013 Global Status Report

15

OECD, International Energy Association (IEA), World Energy Outlook 2012, REN

21 Renewables 2013 Global Futures Report

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

3 | Taxes and incentives for renewable energy

Global investment in

renewable energy production

In 2012, global investments in

renewables reached USD244 billion.

This figure represents a decrease of

12 percent.

16

Investment levels in 2013

have followed this trend. As of Q1

2013, global investment in renewables

reached only USD40 billion, the lowest

in any quarter since Q1 2009 and a

decrease of 36 percent from the final

quarter of last year and 24 percent

below the first quarter of 2012.

17

This decline can be explained by several

factors, starting with uncertainty

about renewables policy in developed

economies. Investments declined

34 percent in the US because of policy

uncertainty, and former champions

for renewables in Europe such as Italy

and Spain saw significant contractions

based on policy changes and cuts in tariff

supports. The decline in investments

was also driven by overcapacity

in the manufacturing supply chain

in North America and Europe.

In addition, dramatically lower prices

for renewable energy have discouraged

investors. Solar prices dropped 30 to

40 percent between 2011 and 2012,

driven mainly by low-cost manufacturing

in China.

18

Wind turbine prices dropped

by 20 to 25 percent in western markets

and by 40 percent in China.

19

Another key trend in renewables

investment for 2012 was the continued

north to south shift toward emerging

markets. In 2007, developed economies

invested 2.5 times more in renewables

than the south. Now the gap has shrunk

to 18 percent, and emerging markets

are on track to surpass the north in

the next few years. Total renewables

investment in developing economies

rose 19 percent in 2012 to USD112

billion, while investment in developed

countries dropped 29 percent to

USD132 billion.

20

China, South Africa,

Morocco, Mexico, Chile and Kenya all

showed sharp increases in investment.

21

Significantly, incentives have been

maintained or increased in many Asian

countries even as they were being

reduced in many developed countries.

According to the REN21 Renewables

2013 Global Status Report, the top five

countries for new capacity investments

in renewable energy in 2012 were China,

the United States, Germany, Japan and

Italy. In KPMG’s Green Tax Index focusing

on fiscal incentives, China ranked

sixth, the United States ranked first,

Germany fifteenth and Japan second.

Italy was not included in this report.

(For additional information,

see appendix A/page 57)

16

Global Trends in Renewable Energy Investments 2013,

Bloomberg New Energy Finance

17

Ibid.

18

Ibid.

19

Bloomberg New Energy Finance, IHS Research

20

Ibid.

21

Op. cit., Global Trends in Renewable Energy Investment 2013

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Taxes and incentives for renewable energy | 4

China:

China was the dominant country in 2012

for investments in renewable energy,

with commitments rising 22 percent to

USD67 billion, representing 27 percent

of global renewables investment.

22

This

surge was due mainly to a spike in solar

investment.

23

Since 2005, China has

increased its renewables investment by

over 300 percent.

The government’s support for

renewables in China includes reduced

corporate income taxes, significant

reductions in value added taxes, feed-

in tariffs, R&D incentives, subsidies

for energy conservation technologies

improvement, and other tax incentives.

In a related note, Chinese companies

have provided nearly USD40 billion

to solar and wind industries in other

countries over the past decade.

24

Most

investments have gone to the US,

followed by Germany, Italy and Australia.

China’s wind industry supports the

domestic market, but the solar industry

relies on the international market for

95 percent of its sales.

25

More on page 16

United States:

The US ranked second in 2012 for

renewables investments, with a total

of USD36 billion. This represents a

drop of 34 percent over the previous

year. Most investment dollars went

to asset finance, while the remaining

portion went to public markets, venture

capital/private equity, corporate and

government R&D and small distributed

capacity.

Suggested strategies to increase the

US investments in renewables involve

a greater alignment of state, federal

and private efforts. At the state-level,

renewable energy portfolio standards

(RPS) and policies like electricity market

design have been proven successful.

These can complement federal

production and investment tax credits.

From the private sector, policies such as

Master Limited Partnerships (MLPs) and

Real Estate Investment Trusts (REITs)

can help provide lower-cost capital.

More on page 53

Germany:

Although Germany led the world in

renewable power per capita for 2012,

26

investments fell 35 percent from

previous year to USD20 billion.

27

Feed-

in tariffs are available in Germany for

wind, solar, geothermal, methane gas

and hydro generation. The government-

owned bank KfW also provides various

subsidies and support programs for

renewables. However, a major shift

away from nuclear plants and the

upcoming elections in September

2013 have introduced a high level of

uncertainty for investors. Feed-in tariffs

are expected to be cut, and other

reductions in incentives are expected.

More on page 22

Japan:

After the Fukushima earthquake, Japan

introduced several significant incentives

to support the move from nuclear to

renewable energy sources. These

include a special depreciation of

30 percent or 100 percent for the

purchase and installation of qualified

renewable energy equipment. In

addition, the government introduced an

incentive for fixed assets tax on certain

renewable energy generation facilities.

Not surprisingly, 2012 investments

in renewables increased 73 percent

over 2011 to USD16 billion.

28

Most

investments were for small-scale solar

PVfacilitiesthatpromiseafasterreturn

on investment. Goldman Sachs Group

Inc. (GS) has announced plans to invest

as much as USD487 million in renewable

energy projects in Japan in the next five

years.

29

Japanese banks and financial

institutions such as Softbank Corp. and

Orix Corp. have also shown considerable

interest in renewables investment.

30

More on page 31

Italy:

The renewable energy sector in Italy is

considered by some to have the highest

potential in the EU.

31

The country has

a well-developed system of incentives

(mainly feed-in tariffs) for renewable

energy generated from solar, wind and

biomass. In particular, the government’s

Renewable Energy Decree, which

entered into force on 29 March 2011,

revises the system of incentives for the

production of electricity from renewable

sources and simplifies the authorization

process for building new plants.

Nevertheless, the prolonged European

nancialcrisis,lowerPVcostsandother

factors have made their impact on the

sector. In 2011, Italy attracted USD29

billion in renewable energy investment,

but asset financing of renewable energy

in 2012 dropped 31 percent as compared

to 2010.

32

Investment from asset finance,

public markets and private equity was

down 26 percent.

33

More on page 28

22

Ibid.

23

Ibid.

24

China invests billions in international renewable energy projects,

WRI Insights, wri.org

25

Ibid.

26

not including hydro

27

Op. cit., Global Trends in Renewable Energy Investment 2013

28

Renewable energy investments shift to developing nations, Bloomberg,

12 June 2013

29

Goldman Sachs Eyes Japan Renewable Energy Investments, Bloomberg,

20 May 2013

30

Ibid.

31

Italy’s Renewable Energy Sector Continues to Attract Investors, According

to Mergermarket, Mergermarket, 9 May 2013

32

Can Italy Keep Its Renewables Investors?, RenewableEnergyWorld.com,

23 July 2013

33

Ibid.

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

5 | Taxes and incentives for renewable energy

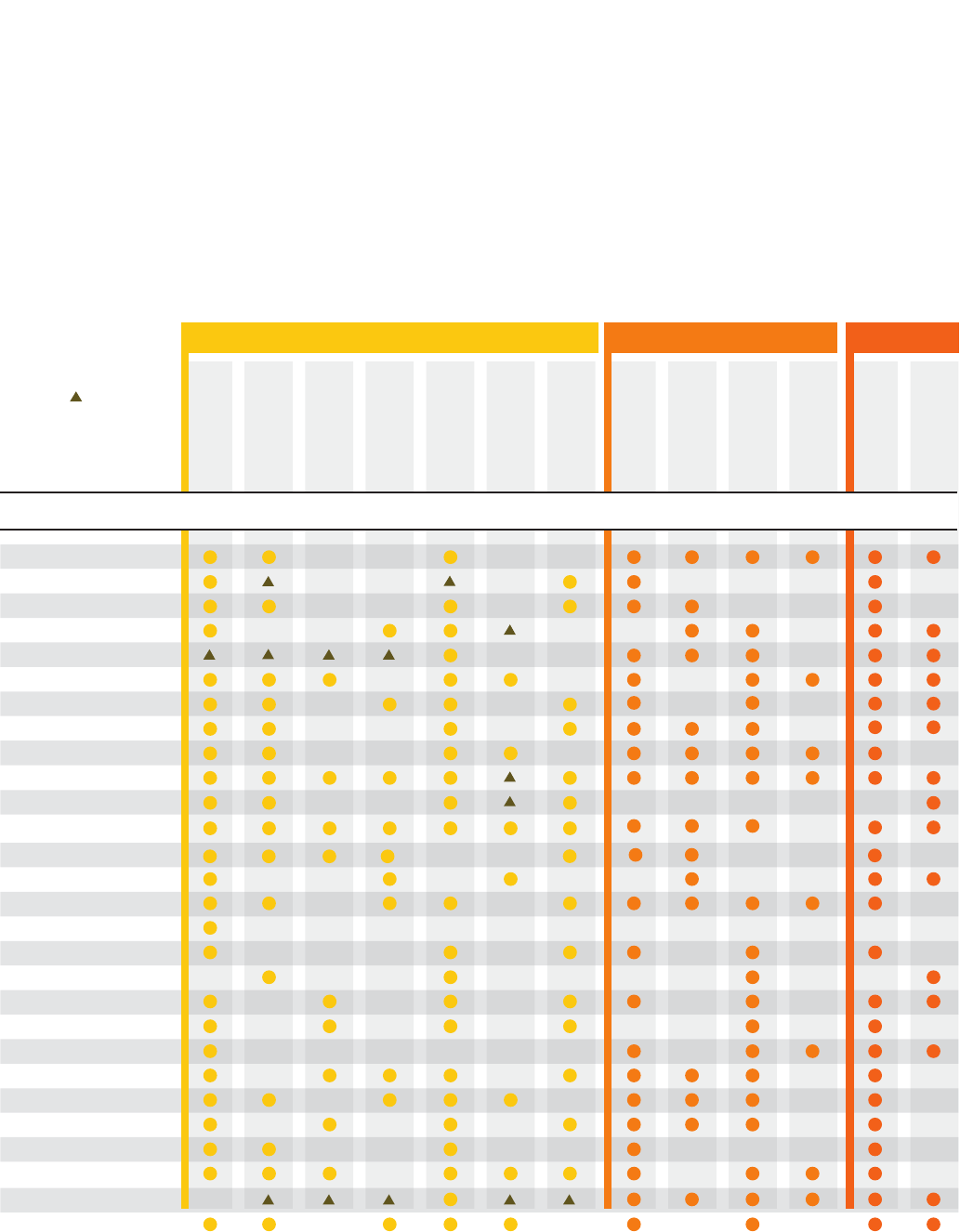

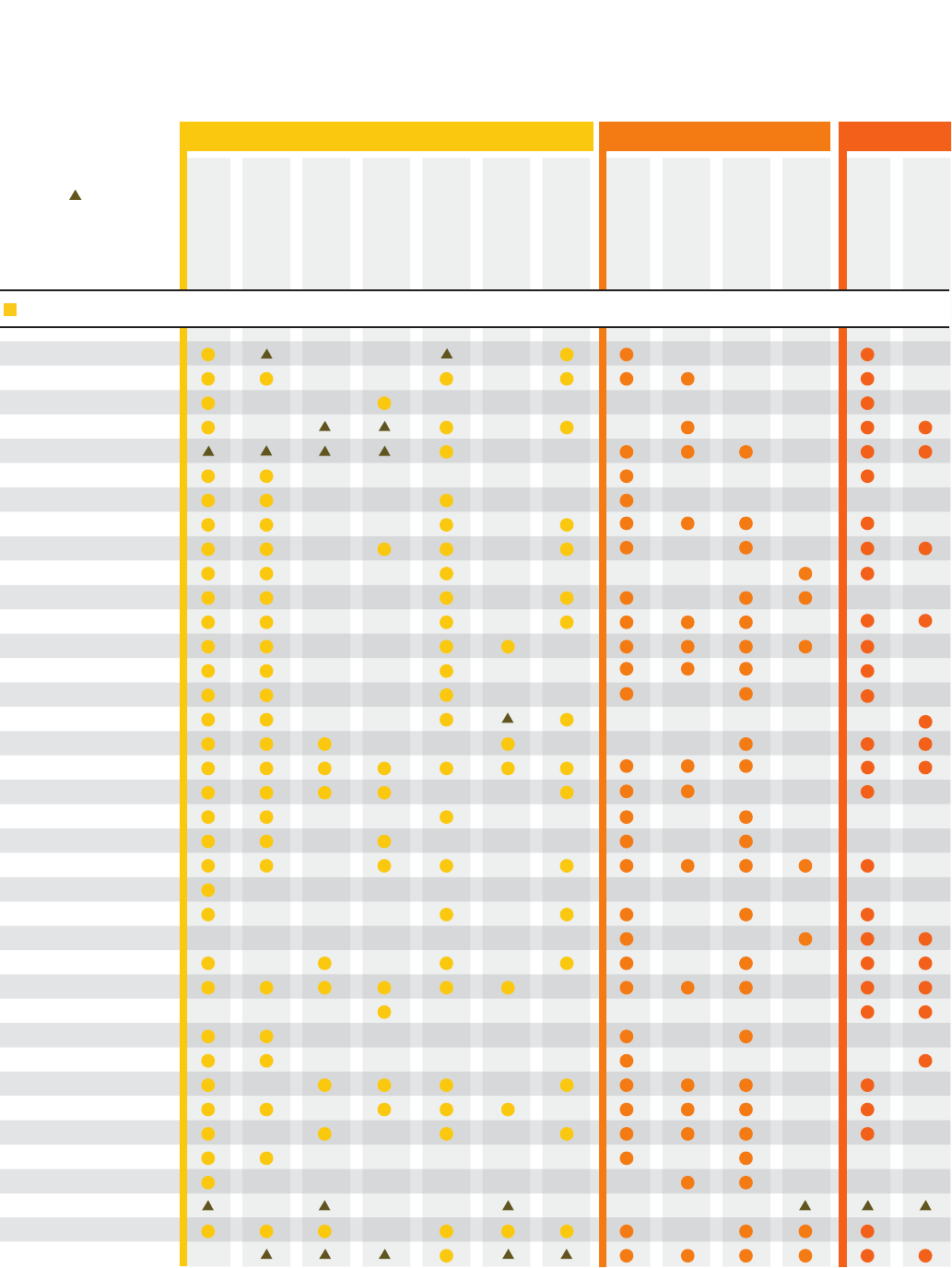

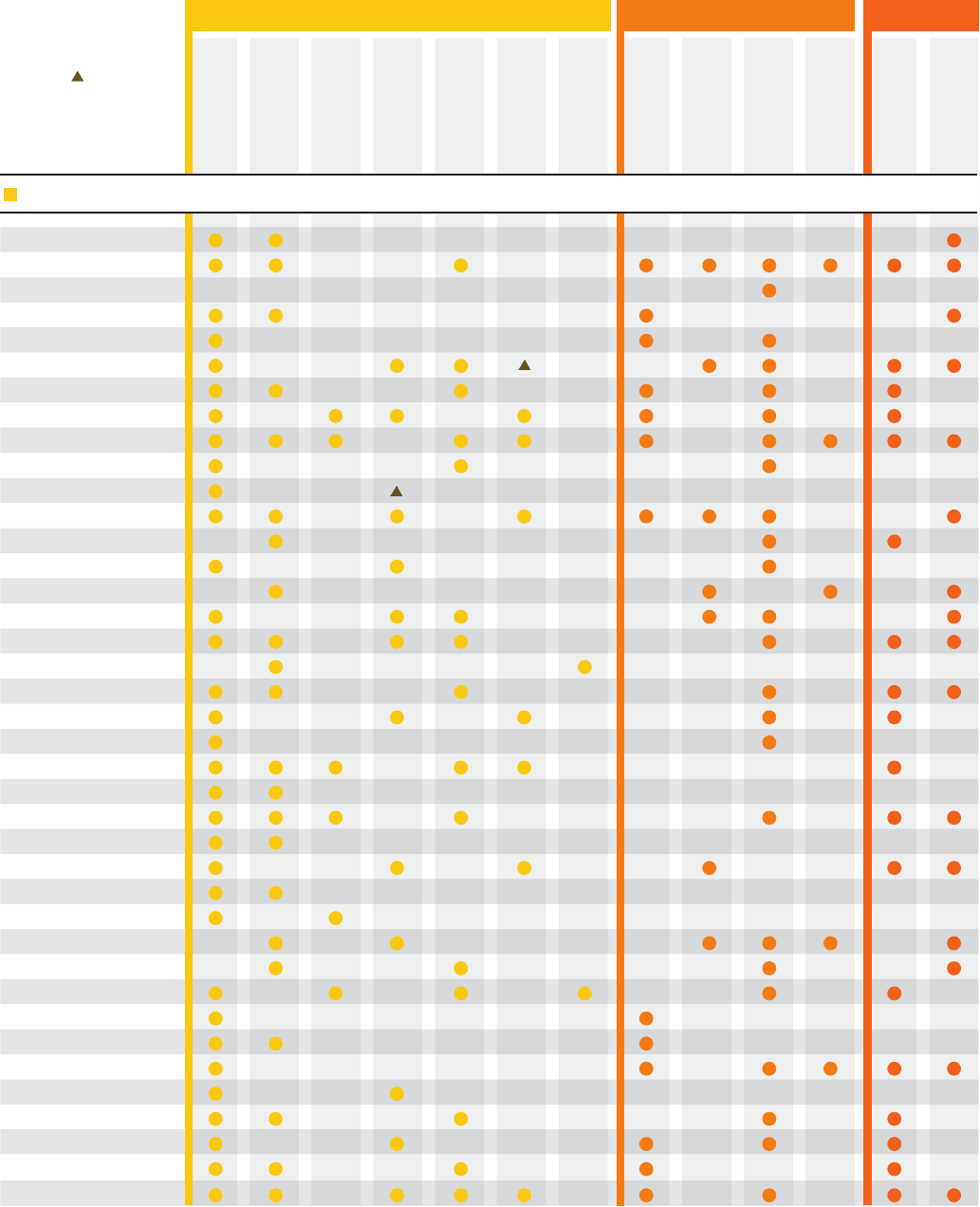

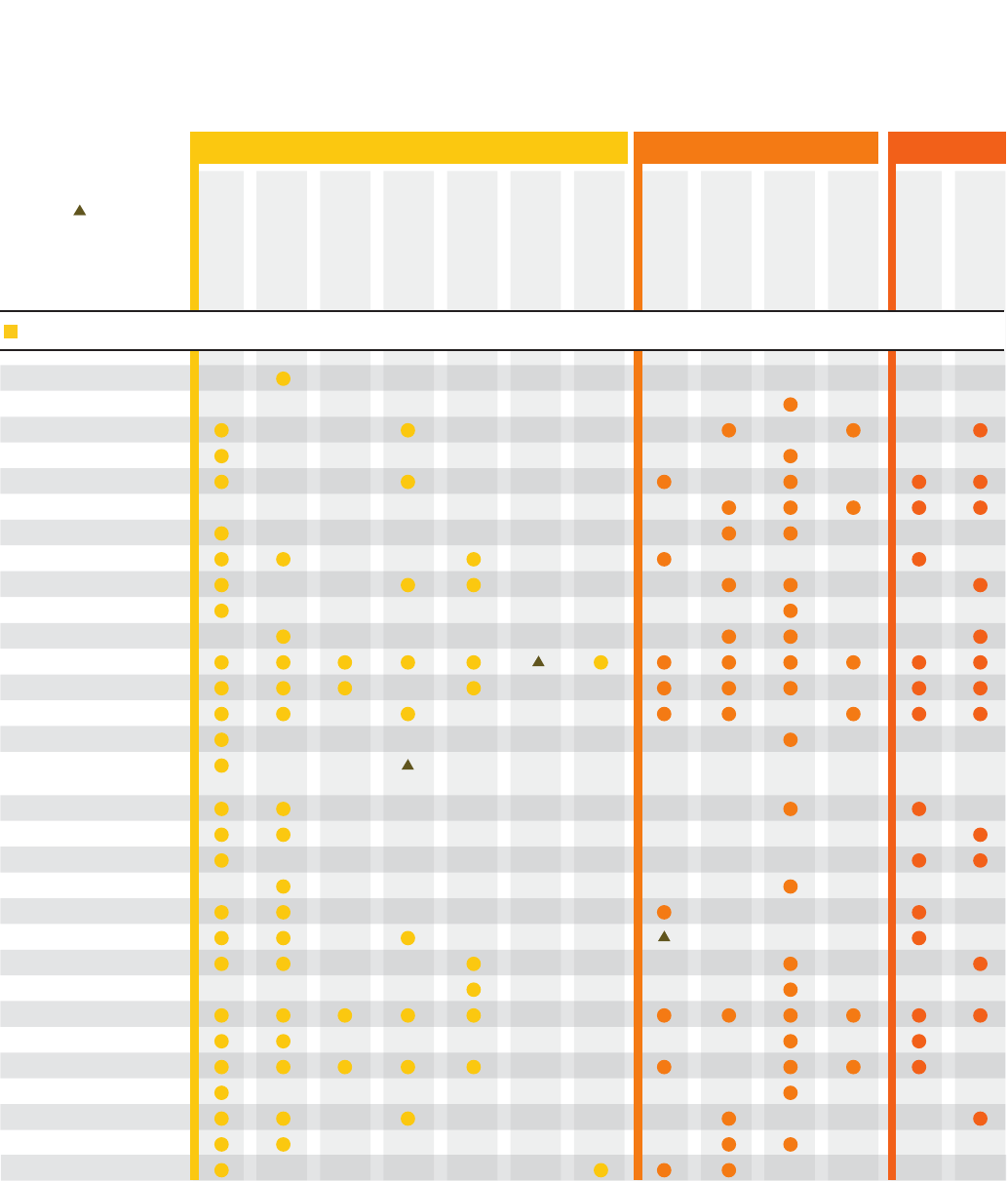

Renewableenergypromotion

policies by country

The following chart is a summary of the support schemes available in the 28 countries that are highlighted in this publication.

Additional details regarding the investment and operating support schemes for each country can be found in the following pages.

Australia

Renewable energy

targets

Feed-in tariff/

premium payment

Electric utility

quota obligation/

RPS

Net metering

Biofuels obligation/

mandate

Heat obligation/

mandate

Tradable REC

Capital subsidy,

grant, or rebate

Investment or

production tax

credits

Reductions in

sales, energy, CO

2

,

VAT or other taxes

Energy production

payment

Public investment,

loans, or grants

Public competitive

bidding/tendering

Austria

Canada

Denmark

France

Germany

Italy

Netherlands

New Zealand

Norway

Poland

South Korea

Spain

34

Sweden

United Kingdom

United States

REGULATORY POLICIES AND TARGETS FISCAL INCENTIVES

PUBLIC

FINANCING

Some states/

provinces within

these countries have

state/provincial-level

policies but there is no

national-level policy.

Argentina

China

Romania

Turkey

Mexico

Peru

South Africa

Brazil

Source: This section is intended only to be indicative of the overall landscape of policy activity and is not a definitive reference. Policies listed are generally those tha

have been enacted by legislative bodies. Some of the policies listed may not yet be implemented, or are awaiting detailed implementing regulations. It is obviously

difficult to capture every policy, so some policies may be unintentionally omitted or incorrectly listed. Some policies may also be discontinued or very recently

enacted. This report does not cover policies and activities related to technology transfer, capacity building, carbon finance, and Clean Development Mechanism

projects, nor does it highlight broader framework and strategic policies – all of which are still important to renewable energy progress. For the most part, this report

also does not cover policies that are still under discussion or formulation, except to highlight overall trends. Information on policies comes from a wide variety of

sources, including the International Energy Agency (IEA) Renewable Energy Policies and Measures Database, the U.S. DSIRE database, RenewableEnergy-

World.com, press reports, submissions from country-specific contributors to this report, and a wide range of unpublished data. Much of the information presented

here and further details on specific countries appear on the “Renewables Interactive Map” at www.ren21.net. It is unrealistic to be able to provide detailed

references to all sources here. REN 21 Renewables 2013 Global Status Report.

t

34

In Spain, the feed-in tariff (FIT) and net metering programmes have been temporarily suspended by Royal Decree for new renewable energy projects; this

does not affect projects that have already secured FIT funding. The Value Added Tax (VAT) reduction is for the period 2010–12 as part of a stimulus package.

India

Ireland

Uruguay

Japan

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Taxes and incentives for renewable energy | 6

Market issues

To help clients address key challenges

in today’s rapidly evolving renewable

energy sector, KPMG member firms

provide services backed by a global

network of resources, information and

experience. The KPMG Energy & Natural

Resources practice has specialists in

the field of renewable energy, based

in key business locations around the

world, acting as a single network. In

each location, KPMG professionals

can offer practical, in-depth, renewable

energy experience. They can also draw

on the KPMG global network of Energy

& Natural Resources practitioners to

provide clients with immediate access

to the latest industry knowledge, skills,

resources and technical developments.

With regular calls and effective

communications tools, we can share

observations and insights, debate new

emerging issues and discuss issues

that are critical to clients’ management

agendas. This global network also

produces publications and commentary

on key issues affecting the sector,

business trends, changes in regulations

and the commercial, risk and financial

challenges of doing business.

KPMG’s ENR Tax Services &

Solutions – engaging the green

agenda

KPMG firms can help you to review

your regulatory and sustainability

business strategies and your energy

and emissions trading objectives.

We can provide tax characteristics

of carbon credits, resolve Clean

Development Mechanism issues, and

define implications of Certified Emission

Reduction forward contracts from both

trading and transfer pricing standpoints.

We can also help you navigate the

wide array of available global and

local government and municipal grant

programs or tax incentives related to

the production and sale and purchase

of alternative energy and green

products. These include feed-in tariffs,

tax holidays, accelerated depreciation,

carbon tax/pricing, trading schemes,

energytaxes,excisetaxesorVAT

in relation to wind, solar, biomass,

biofuels, geothermal and hydropower

sources, as well as increased energy

efficiencies, smart-grid technologies,

and carbon capture and storage

technologies.

Due to the impact of these incentives

and taxes on your investment decisions,

KPMG firms can factor them into

tailored due diligence and tax modeling

services. These services apply not only

to production or sale/purchase of green

goods but also to green investments

and financing arrangements.

KPMG’s Global ENR Tax network

includes professionals who specialize in

these tax practice areas:

• FinancialServicesTax

• GlobalIndirectTax

• GlobalTransferPricingServices

• InternationalCorporateTax

• Mergers&Acquisitions.

Investing in the sector

KPMG member firms invest significant

time and resources in deepening our

understanding and knowledge of the

sector. This enables us to provide clients

with strategic and insightful services

that are tailored to their specific needs

and based on an understanding of their

challenges.

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

7 | Taxes and incentives for renewable energy

Argentina

Support schemes

Investments and other subsidies

Support is available for renewable

energy sources including biofuels, solar,

wind, hydro and geothermal, among

others.

At the local tax level:

• Anticipatedvalueaddedtax(VAT)

refunds for the new depreciable

property (except for automobiles)

included in the project.

• Acceleratedincometaxdepreciation.

(filing two claims for the same project

are not allowed).

The property used for the project will

not be part of the minimum presumed

income tax taxable base. In addition,

biofuel producers will not be subject to

the hydric infrastructure tax, the tax on

liquid fuels and the gas oil tax for the

amount of fuel that is marketed in the

national territory.

At the provincial level:

• realestatetaxexemption

• stamptaxexemption

• turnovertaxexemption/deferral

• taxstability.

The type of benefit depends on the

geographic area in which the renewable

energy plant operates, so the plant’s

specific location must be supplied for a

proper tax classification.

Operating subsidies

Subsidiesatthenationallevel:

• Wind:0.015Argentinepeso

(ARS)/ kWh

• Solar:0.9ARS/kWh

• Hydroforlessthan30MWinstalled

capacity: 0.015 ARS/kWh

• Other:0.015ARS/kWh.Several

provinces have different incentive

feed-in tariffs according to the kind of

energy they want to promote.

Quota obligation

The aim is to reach a contribution of

sources of renewable energy equal

to eight percent of the total national

consumption of electric energy within

a term of 10 years, starting in 2006, the

effective date of the regime.

Quota obligations also include the

use of fossil fuel mixed with at least

five percent of biofuels, including

biodiesel and bioethanol.

Additional information

The following authorizations are

required for the construction of

renewable energy plants:

• authorizationtousetheland

• environmentalimpactstudy

• approvalbytheEnergySecretariat

• biddingoffersubmittedthrough

the Program of Electric Generation

through Renewable Energies

(Programa Generación Renovable or

GENREN).

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Taxes and incentives for renewable energy | 8

Australia

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Support schemes

Investments and other subsidies

Australia’s clean energy sector is

currently experiencing significant

change in the wake of the Australian

government’s introduction of the

Securing a Clean Energy Future Climate

Change Plan (the Plan). The Plan has

initiatives in four key areas – carbon

pricing, renewable energy, energy

efficiency and land management. The

government has released numerous

federal funding initiatives within the

Plan, many of which are applicable

to renewable energy. There are also

a number of policies, programs and

incentives outside of the Plan, with

key initiatives specifically related to

renewable energy that are described

below.

Carbon Price Mechanism (CPM)

Central to the Plan is the introduction

of a CPM. Revenue generated from

the CPM will be invested to alleviate

the impact of price increases, support

more jobs and encourage innovations

addressing climate change. Enhanced

support for renewable energy is

expected to drive innovation and

investment into clean technologies

and clean energy R&D, demonstration,

deployment and uptake.

The carbon price is being introduced in

a two-step process, starting with a fixed

price period that runs from 1 July 2012

to 30 June 2015 before transitioning to

an emissions trading scheme. In the

fixed price stage the carbon price will

start at Australian dollar (AUD) 23 per

tonne and rise by 2.5 percent a year in

real terms. From 1 July 2015 onwards,

the price will be set by the market, with

the number of permits issued by the

government each year to be capped. The

carbon price was passed by parliament

on 8 November 2011 and commenced

on 1 July 2012.

Australian Renewable Energy

Agency (ARENA)

ARENA is tasked with managing

AUD3.2 billion of financial assistance

for renewable energy projects and

initiatives promoting the R&D,

demonstration, commercialization

and deployment of renewable energy

projects. The availability of this

funding is expected to improve the

sector’s long-term competitiveness

and drive down its costs in an

Australian context. Approximately

AUD2.2 billion of ARENA’s funding

is currently uncommitted and will be

available to support future projects

in the renewable energy sector.

ARENA incorporates and has

responsibility for overseeing

renewable energy initiatives previously

administered separately through a

range of bodies including the Australian

Centre for Renewable Energy (ACRE),

Solar Flagships Program, Australian

Solar Institute (ASI), Low Emissions

Technology Demonstration Fund,

Renewable Energy Demonstration

Program,RenewableEnergyVenture

Capital Fund, Australian Biofuels

Research Institute, Geothermal Drilling

Program and the Second Generation

Biofuels Research and Development

Program. ARENA also has accountability

for administering unallocated funding.

Listed below are initiatives which are

currently open or in planning phases

where additional funding is expected to

be announced.

EmergingRenewablesProgram

(ERP)

The ERP is focused on supporting

renewable energy technology at the

development, demonstration and

supported commercial stages of the

innovation chain. Ultimately the aim is

to lower the cost of energy produced

by renewable energy technologies to

a point where they are better able to

compete with traditional fossil-fuel

technologies. Funding totalling AUD126

million is available under two categories:

• Projects – Offers funding for

renewable energy and enabling

technologies and products as they

move through the technology

innovation chain. The application

process is undertaken in two phases,

with funding allocations expected to

fall within the range of AUD2 million

to 30 million.

• Measures – Offers funding for

initiatives that involve a renewable

energy industry capacity building

activity, skills development activity

or a preparatory activity for an ACRE

Project. The application process

is undertaken in one phase and is

expected to fund up to AUD2 million,

with a maximum funding pool of

AUD10 million.

Of the total funding pool of AUD126 million:

• AtleastAUD40millionwillbe

allocated to assist the development

of renewable energy and enabling

technologies with the potential

to contribute to the generation of

large-scale base load power such

as wave, geothermal and enabling

technologies.

• AfurtherAUD26.6millionwillbe

allocated specifically to assist the

geothermal energy sector.

RegionalAustralia’sRenewables

(RAR)

ARENA has also launched a new

strategic initiative, the RAR program,

which aims to demonstrate the viability

of renewable energy in regional and

remote locations. It will support

the deployment of commercially

prospective renewable energy

technologies, both generation and

enabling, in off-grid and edge-of-grid

situations. The RAR program has

sought community consultation and is

expected to be formally launched in the

first half of 2013, with funding running

for two to three years.

9 | Taxes and incentives for renewable energy

RenewableEnergyVenture

CapitalFund

The Southern Cross Renewable

Energy Fund is a 13-year, AUD200

million venture capital fund, operated

bySouthernCrossVenturePartners.

The fund was established under the

Australian government’s AUD100 million

RenewableEnergyVentureCapitalFund

(REVC).Thegovernment’scontribution

has been matched by an additional

AUD100 million contributed by Softbank

ChinaVentureCapital.

With offices and staff located in

Sydney, Palo Alto and Shanghai, the

fund makes selected investments

in Australian renewable energy

companies, providing capital and

assisting with the management skills

they need to commercialize their

technologies and succeed in

domestic and overseas markets.

Opportunities previously funded

by the ASI

ARENA has committed support for

programs previously administered by

the ASI, including the United States-

Australia Solar Energy Collaboration

Strategic Research Initiative as well as

solar Ph.D. scholars and postdoctoral

fellows following the success of ASI’s

Skills Development Program.

CleanEnergyFinanceCorporation

(CEFC)

The government has established the

CEFC through a financial commitment

of AUD10 billion to overcome capital

market barriers that hinder the

financing, commercialization and

deployment of renewable energy,

energy efficiency and low emissions

technologies. The CEFC will be

responsible for investing in firms and

projects that utilize these technologies

as well as manufacturing businesses

that focus on producing the inputs

required.

The CEFC began operations on 1 July

2013 and offers complementary

financing alongside private sector

financing for renewable energy and

clean energy enabling technologies.

Funding will be allocated over a period

of five years, with AUD5 billion for

renewable energy and technology

including geothermal, wave energy and

large scale solar power generation. The

remaining AUD5 billion will be allocated

to the general clean energy stream

which may also include renewable

energy.

The CEFC is intended to be

commercially oriented and make a

positive return on its investment. In its

early stages the CEFC will be offer loans

on concessional commercial terms,

with each agreement being considered

individually. As the fund matures, the

CEFC may choose to offer alternate

funding arrangements, including

mezzanine finance and other equity-

based funding arrangements.

EthanolProductionGrants(EPG)

The EPG program will support the

production and deployment of ethanol

as a sustainable alternative transport

fuel in Australia. The program provides

support via a full excise reimbursement,

at a rate of 38.143 cents per litre,

to ethanol producers for ethanol

produced and supplied for transport

use in Australia from locally derived

feedstocks. The program and grants

are administered by the Department of

Resources, Energy and Tourism.

R&DTaxIncentive

The major mechanism and program

for fostering innovation is a tax-based

scheme rewarding expenditure on

R&D activities. The R&D Tax Incentive

scheme is a broad-based program

accessible to all industry sectors. The

R&D scheme has recently undergone

a significant change, transitioning from

the R&D Tax concession to the R&D Tax

Incentive. In many instances, activities

conducted as a part of renewable

energy development may be eligible

for the R&D tax incentive. The program

offers two tiers of incentive based on

the turnover of the company in question:

• A45percentrefundabletax

offset (equivalent to a 150 percent

deduction) for eligible entities with a

grouped turnover of less than AUD20

million per annum.

• Anon-refundable40percenttaxoffset

(equivalent to 133 percent deduction)

for all other eligible entities. Unused

non-refundable offset amounts may

be able to be carried forward to future

income years.

The R&D Tax Incentive is an entitlement-

based, self-assessment program.

Registration of activities, via the R&D

application, is required within 10 months

of the relevant financial year end.

Operating subsidies

Feed-intariff

There are no national based feed-in

tariffs. However, a number of state-

based initiatives exist for small-scale

generation. The Australian Capital

Territory (ACT) has a Large Scale Feed-

in Tariff Scheme (the Scheme) which

provides the ACT government with

power to grant feed-in tariff entitlements

up to 210 MW of generation capacity.

The first tranche of capacity released

under the ACT provided industry with

an opportunity to compete for the

establishment of up to 40 MW of solar

generation (minimum 2 MW generating

system capacity). Applications for the

40 MW tranche are closed, but further

tranches are expected.

Quota obligation

20 percent by 2020.

Additional information

In addition to the funding initiatives

described above, the government

also has a number of policy levers and

numerous other programs.

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Taxes and incentives for renewable energy | 10

Austria

35

For applications filed in 2012

Support schemes

Investments and other subsidies

Small solar plants

Less than 5 kWp investment subsidies

are granted for the plants, sufficient for

them to achieve a six percent capital

yield.

Waste liquor plants

Maximum 30 percent of the investment

(not including real estate costs)

• upto100MW:EUR300/kW

• 100MWto400MW:EUR180/kW

• morethan400MW:EUR120/kW

Small hydro plants

• maximum30percentofthe

investment for 500 kW capacity:

up to EUR1500/kW

• maximum20percentofthe

investment for 2 MW capacity:

up to EUR1000/kW

• maximum10percentofthe

investment for 10 MW capacity:

up to EUR400/kW

• inbetweenthesesetpercentages,

the maximum is calculated via linear

interpolation.

Medium hydro plants (<10 MW)

• maximum10percentofthe

investment

• maximumEUR400/kWandmaximum

EUR6 million per plant

Operating subsidies

Feed-intariff

35

Wind energy:

• cents(ct)9.45/kWh

Solar:

In buildings:

• 5kWpto500kWp:ct18.12/kWh

In open space:

• 5kWpto500kWp:ct16.59/kWh

Geothermal:

• ct7.43/kWh

Sewage gas

• ct5.94/kWh

Landll gas

• ct4.95/kWh

Compact biomass (such as forest

woodchips or straw)

• ct8.9/kWhtoct14.00/kWh,

depending on the production

capacity (declining tariff)

Waste with high biogenic contingent

• Sameasforcompactbiomass,minus

25 percent

Liquid biomass

• ct5.74/kWh;surplusofct2/kWhfor

production in an efficient power-heat

cogeneration

Biogas from agrarian production

• ct12.93/kWhtoct19.5/kWh,

depending on the production capacity

(declining tariff)

Additional information

Legal

The feed-in tariffs are regulated by the

law for the promotion of electricity

production from renewable energy

resources (“Ökostromgesetz 2012”).

The concrete feed-in tariffs have to be

determined each year by a decree from

the Ministry of Economics.

Duration of the feed-in-tariffs

15 years for liquid and concrete

biomassorbiogas;13yearsforallother

renewable technologies.

Administrative procedures

Applications have to be filed with the

Renewable Energy handling Center

(“Ökostromabwickklungstelle,” http://

www.oem-ag.at/).

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

11 | Taxes and incentives for renewable energy

Brazil

36

Producers and importers are legal entities that are beneficiaries of concessions or authorizations from the National Petroleum Agency (ANP). They are registered as

producers or importers of biodiesel in the Special Register held by the Brazilian Internal Revenue Service.

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Support schemes

Investments and other subsidies

Taxes over revenue and imports

(PISandCOFINS)

• aspecialtaxregimeisapplicablein

Brazil for producers and importers

of biodiesel,

36

which includes two

programs: the Social Integration

Program (Programa de Integração

Social or PIS) and the Contribution to

the Social Security Fund (Contribuição

para o Financiamento da Seguridade

Social or COFINS). The PIS and

COFINS taxes due are definitive,

meaning that the resale of biodiesel

by wholesalers, distributors and

retailers is not subject to PIS and

COFINS. Under this tax regime, the

producers and importers can opt for:

– a 6.15 percent PIS rate and a

28.32 percent COFINS rate

levied on gross revenues derived

frombiodieselsales;or

– a fixed value of PIS and COFINS

by cubic meter of commercialized

biodiesel Brazilian real (BRL) 26.41

and BRL121.59, respectively.

Producers opting for the fixed

value can obtain certain reductions

and exemptions of the amounts

due, depending on the supplier of

raw material or input applicable

to the production (for example,

acquisition from castor bean

producers or from family farmers).

Moreover, producers of biodiesel

under a non-cumulative regime

of PIS and COFINS are able to

offset 4.625 percent of presumed

credit on acquisition of inputs

from individuals or legal entities

that supply agribusinesses or

agribusiness cooperatives.

• Thesugarcanesalesforethanol

production are exempt from PIS and

COFINS, provided that the tax payer

is under the non-cumulative regime.

• Thereisaspecialtaxregime

for producers, importers and

distributors of ethanol. The producers

and importers may opt for:

– a 1.5 percent PIS rate and a

6.9 percent COFINS rate levied

ongrossrevenueofethanolsales;

– a fixed value of PIS and COFINS

by cubic meter of commercialized

ethanol – BRL8.57 and BRL39.43,

respectively, up to 31 August 2013.

Recently, the Brazilian government

edited Decree 7.997/13, which sets

forth that, from 1 September 2013,

the fixed value of PIS and COFINS

by cubic meter of commercialized

ethanol shall be increased to BRL21.43

and BRL98.57, respectively.

Despite this, the Brazilian government

enacted Provisional Measure 613

that grants to the producers and

importers a presumed credit in the

same values, which leads to a practical

effect of zero rate of PIS and COFINS.

Also, the taxpayers may opt for this

new fixed value and the presumed

credit in advance (from 8 May 2013).

When it comes to distributors of

ethanol, the options are (depending on

the option of the producer or importer).

– a 3.75 percent PIS rate and a

17.25 percent COFINS rate levied

ongrossrevenueofethanolsales;

– a zero rate for the fixed

PIS and COFINS.

• Ethanolsalescarriedoutbyretailers

and sales negotiated through the

Future & Commodities Exchange (Bolsa

de Mercadorias e Futuros or BM&F)

are not subject to PIS and COFINS.

FederalandstateVAT(IPIandICMS)

• Biodieselandethanolsalesare

not subject to the Industrialized

Products tax (Imposto Sobre

Produtos Industrializados or IPI).

• Equipmentusedintherenewable

energy generation process is

generally exempted from the IPI.

• TheStateValue-AddedTaxon

Sales and Services (Imposto Sobre

a Circulação de Mercadorias e

Serviços or ICMS) can possibly

be exempted for some products

used for biodiesel or ethanol

production. In addition, the ICMS

calculation basis may be reduced

for interstate operations related to

ethanol and biodiesel production

and distribution. This reduction

depends on individual state law.

• Inthesameway,operations

involving equipment used in the

generation of wind and solar

energy can possibly be ICMS tax-

exempt until 31 December 2015.

Contribution for Intervention in

theEconomicDomain(CIDE)

• Ethanolsalesarenotsubject

to Contribution for Intervention

in the Economic Domain

(Contribuição de Intervenção no

Domínio Econômico or CIDE).

Operating subsidies

Feed-intariff

Wind: N/A

Biomass: N/A

Hydro: N/A

Brazil currently has no feed-in tariff policy.

Taxes and incentives for renewable energy | 12

Additional information

Brazil is considered the world’s sixth

largest investor in renewable energy.

37

Nationwide, 44.1 percent of the Internal

Energy Supply (Oferta Interna de

Energia or OIE) is renewable,

38

whereas

the world’s average is 20.3 percent.

39

Furthermore, the National Bank for

Economic and Social Development

(Banco Nacional do Desenvolvimento

Econômico Social or BNDES) provides

a variety of financial programs

to stimulate the production of

renewable energy. The development

of the renewable energies in Brazil

is increasing, and almost half of the

energy consumed in Brazil is now

generated by renewable sources.

The actual scenario is very

advantageous for renewable energy.

The government expectations are that

renewable energy may be responsible

for 18 GW out of a total increase of

63 GW in the total installed capacity of

the segment over the next 10 years.

40

According to the Ministry of Mines

and Energy, Brazil is especially well

situated for becoming a major producer

of biodiesel. The country contains a vast

amount of arable land, much of which

has the right soil and climate for growing

a variety of oilseeds.

The growth of biodiesel as an alternative

energy source in Brazil is supported

by Federal Law 11.097/05, which

mandates a minimum of five percent of

biodiesel to be mixed with diesel and

the monitoring of this mixture in the

marketplace. This law also supports the

funding of R&D for biodiesel and other

energy sources, as well as all phases of

production, including the acquisition of

equipment and technology.

In a related matter, Brazil is one of the

most promising countries for wind

energy.

41

The first wind energy auction

was held at the end of 2009, in which

the government bought 1805 MW of

wind energy at a price of BRL148.39/

MWh. Encouraged by the success of

this auction, the government continues

to hold auctions on an annual basis.

Additional benefits not yet in force

Several other incentives being

discussed in the Brazilian scenario are

also worth mentioning:

The Brazilian Commission of

Infrastructure Services (CI) approved

PLS 311/09, a federal project law that

establishes the Special Regime of

Taxation to encourage the development

and generation of electric power from

alternative sources (Regime Especial

de Tributação para o Incentivo ao

Desenvolvimento e à Produção de

Fontes Alternativas de Energia or

REINFA). This project foresees several

tax benefits such as exemptions of

PIS and COFINS, import taxes and IPI

for companies operating under the

regime. It is important to emphasize

that this is not a law in force, yet. At the

present time, it is still awaiting internal

procedures in the Federal Senate.

After COP-15, Brazil formalized

its commitment to reduce carbon

emissions and increased its goal by

2.8 percent. Under the National Policy

on Climate Change (law 12.187/09),

Brazil has pledged to reduce carbon

emissions 38.9 percent by 2020.

According to this law, Brazil could grant

several tax benefits to encourage the

use of renewable energy. At this point in

time, these benefits have not yet been

implemented.

Recently, the government announced

the creation of a program of incentives

to the ethanol sector. This program

involves several benefits to this market

that will be implemented soon:

• CreationofalineofcreditofBRL6

billion for the production and storage

of sugarcane and ethanol with

reduced interests.

• Increasingofthepercentageof

ethanol to be mixed with gasoline

from 20 percent to 25 percent.

• Reductionofchemicalinputcosts,

by diminishing the chemical industry

costs with the increasing of its PIS

and COFINS credits.

Finally, other general benefits that

are not specific to renewables may

apply, such as the Special Incentives

Program for Infrastructure Development

(Regime Especial de Incentivos para

o Desenvolvimento da Infra-Estrutura

or REIDI), SUDAM/SUDENE incentives,

and technology innovation. Each one

has its requirements for application and,

in some cases, depends on government

approval.

37

Global Trends in Renewable Energy Investment 2012 – UNEP

38

Energetic National Balance (Balanço Energético Nacional) 2012

39

United Nations Environment Programme – 2012

40

Brazilian government website, 2013

41

GLOBAL Wind Energy Outlook of 2012

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

13 | Taxes and incentives for renewable energy

Canada

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Support schemes

Federalinvestmentsandother

subsidies

The Government of Canada has

committed that Canada’s total

greenhouse gas (GHG) emissions be

reduced by 17 percent from 2005 levels

by 2020 and that 90 percent of Canada’s

electricity be generated from sources

that do not produce GHG pollution by

2020. Here is a summary of incentives

and grants that the federal government

has invested in support of these goals.

Income tax incentives

Accelerated Capital Cost Allowance

(ACCA)

Advantageous ACCA rates are available

for certain types of assets used for

clean energy generation and energy

conservation:

• Class43.1(30percentdeclining

balance basis) for certain clean energy

generation and energy conservation

equipment.

• Class43.2(50percentdeclining

balance basis) for certain equipment

described in Class 43.1 that is

acquired on or after 23 February

2005 and before 2020 that is used for

clean energy generation and energy

conservation and meeting higher

efficiency standards.

• Recentfederalbudgetscontinueto

expand the list of equipment that

qualifies for an ACCA. The current

eligible equipment includes:

– electricity

– high-efficiency cogeneration

equipment

– small hydroelectric facilities

– wind turbines

– fuel cells

– wave and tidal power equipment

– photovoltaic(PV)equipment

– equipment generating electricity

from geothermal energy

– equipment generating electricity

from eligible waste fuel.

– thermal energy

– active solar equipment

– district energy equipment that

distributes thermal energy from

cogeneration

– heat recovery equipment used

in electricity generation and

industrial processes

– ground source heat pump

equipment

– equipment generating heat

for industrial processes or

greenhouses, using an eligible

waste fuel.

– fuels from waste

– equipment that recovers landfill

gas or digester gas

– equipment used to produce

biogas through anaerobic

digestion

– equipment used to convert

biomass into bio-oil.

• The2013budgetproposestobroaden

the eligible equipment in Class 43.2

to include

– Equipment used to produce biogas

using pulp and paper waste and

waste water, beverage industry

waste and wastewater, and

separated organics from municipal

waste.

– A broader range of cleaning and

upgrading equipment used to

convert eligible gases (biogas,

landfill, digester) into biomethane.

Canadian Renewable and Conservation

Expense (CRCE)

To promote development and

conservation of sources of renewable

energy, many start-up expenditures on

renewable projects can be grouped in a

CRCE pool. CRCE can include intangible

expenses such as feasibility studies,

negotiation, regulatory, site approval

costs, site prep and testing, etc. CRCE

can also include test wind turbines that

are part of a wind farm, on projects

where 50 percent or more tangible

costs are reasonably expected to be

included in Class 43.1 or 43.2 ACCA.

CRCE is fully deductible in any year, can

be carried-forward indefinitely or can

be transferred to investors through the

flow-through share rules.

Scientific Research & Experimental

Development (SR&ED) Program

The SR&ED Program is a federal tax

incentive program administered by

the Canada Revenue Agency that

encourages Canadian businesses of all

sizes, and in all sectors, to conduct R&D

in Canada. Companies, including those

carrying on business in clean energy

generation, may be entitled to claim an

Investment Tax Credit (ITC) if they incur

eligible R&D expenditure. The tax credit

is based on money already committed

and spent by the company. The program

is the single largest source of federal

government support for industrial R&D,

returning as much as a 35 percent

federal cash refund.

Sustainable Development

Technology Canada (SDTC)

SDTC plays a significant role in

bridging the gap between research

and commercialization of clean

technologies. It does this by fast-

tracking clean technologies through

their development and demonstration

phases, in preparation for

commercialization. SDTC is an arm’s-

length foundation that was created

by the Federal government to invest

Canadian dollar (CAD)1.09 billion in

innovative technologies and projects

that deliver economic, environmental,

and health benefits to Canadians.

Taxes and incentives for renewable energy | 14

Backed by CAD590 million in funds,

SDTC supports projects that address

climate change, air quality, clean water

and clean soil. The CAD500 million

NextGen Biofuels Fund supports the

establishment of first-of-kind, large

demonstration-scale facilities for

the production of next-generation

renewable fuels.

SDTC acts as the primary catalyst in

building a sustainable development

technology infrastructure in Canada. The

SDTC portfolio is currently comprised

of 245 clean technology projects, for a

total value of CAD2.1 billion, of which

over CAD1.5 billion is leveraged primarily

from the private-sector. In February

2013, SDTC announced its 22nd call

for applications, which was open until

17 April 2013

ecoENERGY

The ecoENERGY program targets

several areas including biofuels, energy

efficiency and renewable energy.

• ecoENERGYforbiofuels:The

ecoENERGY for Biofuels initiative

has a budget of CAD1.5 billion

over nine years to boost Canada’s

production of biofuels. The program

runs from 1 April 2008 to 31 March

2017, and recipients will be entitled

to receive incentives for up to seven

consecutive years.

• ecoENERGYforRenewablePower:

The ecoENERGY for Renewable

Power initiative has a budget of

approximately CAD1.4 billion over

14 years to encourage using

renewable energy sources to create

electricity. The program runs from

1 April 2007 to 31 March 2021. There

are no new agreements signed

after31March2011;however,many

projects with existing contribution

agreements will still receive

payments up until 31 March 2021.

Provincialinvestmentsandother

subsidies

Bioenergy Producer Credit Program

– Alberta

To expand Alberta’s bioenergy sector,

the Bioenergy Producer Credit Program

was established to provide production

subsidies for a variety of bioenergy

products, including renewable fuels,

electricity, and heat using waste

such as manure and wood chips. In

the 2013 budget, the Government of

Alberta cancelled future rounds of the

Bioenergy Producer Credit Program.

However, the government will still be

honouring payments to existing grant

agreements. The program is valid for

bioenergy production from 1 April 2011

to 31 March 2016.

Carbon Capture and Storage (CCS)

fund – Alberta

The Alberta government has

committed CAD2 billion to advance

CCS technology. Approved projects can

receive a maximum of 75 percent of

the total incremental cost to capture,

transport and store CO

2

. A maximum

of up to 40 percent of the approved

funding will be distributed during

the design and construction stage

based on achieved milestones and

up to an additional 20 percent of the

approved funding will be granted upon

commercial operation. The remaining

40 percent of the funding will be

provided as CO

2

is captured and stored

over a maximum period of 10 years.

The government of Alberta has awarded

funding for two projects from its CAD2

billion CCS fund.

• AlbertaCarbonTrunkLine(CAD495

million)

• ShellQuest(CAD745million)

Innovative Energy Technologies

Programs (IETP) – Alberta

The Innovative Energy Technologies

Program (IETP) supports the Provincial

Energy Strategy (PES), which identifies

the need for innovation, research and

technology development. Announced

in 2004, the IETP supports innovative

technology development in the

production of Alberta’s oil, oil sands, and

gas resources. It also supports finding

commercial technical solutions to the

gas-over-bitumen issue to allow the

efficient and orderly production of both

resources. Over time, program costs

will be recovered through additional

recoverable reserves and increased

royalties. Successful applicants in the

program are provided with royalty

adjustments up to a maximum of

30 percent of approved project costs.

The industry must provide the remaining

70 percent or more of total project

costs. The total industry/government

commitment to important new

technologies, assuming full subscription

of the program, will be more than

CAD800 million.

Innovative Clean Energy Fund (ICE) –

British Columbia

The Innovative Clean Energy Fund

encourages the development of

new sources of clean energy and

technologies and supports pre-

commercial energy technology or

commercial technologies not currently

used in British Columbia. Since 2008,

there are 62 projects with a total

amount of CAD77 million that have been

approved throughout British Columbia.

SR&ED tax credit – All provinces

Variousprovincesproviderefundable

and/or non-refundable investment

tax credits (ITC) worth between

10 percent and 15 percent of annual

eligible expenditures (depending on the

particular province) for all corporations

that do business through a permanent

establishment situated in that province.

Eligible expenditures are generally those

that qualify for federal ITC purposes

and are generally capped at a maximum

annual credit.

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

15 | Taxes and incentives for renewable energy

Operating subsidies

There are no feed-in tariffs and quota

obligations at the federal level but they

are implemented in some provinces.

Quota obligation – Alberta

The province of Alberta requires

facilities that emit more than 100,000

tonnes of GHG emissions a year to

reduce their emissions intensity by

12 percent as of 1 July 2007. Emitters

have four choices for compliance with

this emissions reduction target:

• makeimprovementstotheir

operations

• purchaseoffsetcreditsfromother

sectors that have voluntarily reduced

their emissions

• payCAD15atonneintotheClimate

Change and Emissions Management

Fund, an arm’s length organization

independent from the government

that invests the funds into initiatives

and projects that support emission

reduction technologies

• purchaseEmissionsPerformance

Credits from facilities that have

reduced their emissions intensity

below the mandatory 12 percent

threshold.

Feed-intariff(FIT)–Ontario

The Ontario FIT program is North

America’s first comprehensive

guaranteed pricing structure for

renewable electricity production, and it

provides a way to contract for renewable

energy generation. It includes

standardized program rules, prices

and contracts for anyone interested

in developing a qualifying renewable

energy project. Prices are designed

to cover project costs and allow for

a reasonable return on investment

over the contract term, and they are

subject to review periodically. Qualifying

renewable technologies include biogas,

renewable biomass, landfill gas, solar

photovoltaic(PV),waterpowerand

wind power. As of 31 January 2013,

there were 1,728 contracts executed to

generate 4,546 MW of electricity.

With the help of the FIT program,

Ontario is on the track to be the first

jurisdiction in North America to replace

coal-fired generation with cleaner

sources of power by the end of 2014.

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

Taxes and incentives for renewable energy | 16

China

Support schemes

Investments and other subsidies

Corporate Income Tax (CIT)

• AreducedCITrateof15percentis

granted to qualified advanced and new

technology enterprises. Applicable

fields include solar energy, wind energy,

biomaterial energy, and geothermal

energy.

• TheCleanDevelopmentMechanism

(CDM) Fund is exempted from CIT on the

following income:

– the portion of Carbon Emissions

Reductions (CERs) proceeds that are

shared by the government

– donations from international

financial organizations

– interest income derived from

capital deposit or national bonds

– donations from domestic and foreign

entities or individuals.

• EnterprisesoperatingCDMprojects

are allowed to deduct before CIT the

CER proceeds that are shared by the

government.

• ThreeyearsCITexemptionisfollowed

by a 50 percent reduction for another

three years of the standard CIT rate

for income derived from specified

CDM projects. These projects

include hydrofluorocarbons (HFC),

perfluorocarbons (PFC), and nitrous

oxide (N2O) projects, starting from

the year in which the revenue from

the transfer of greenhouse gas (GHG)

emission reductions is first received.

According to the new Administrative

Measures Governing the Operation

of CDM Projects in 2011, any project

companies, except for the 41 state-

owned enterprises listed, shall apply for

approval with the National Development

and Reform Commission (NDRC) at the

provincial level first. Then the commission

would submit preliminary review

opinions to the central NDRC for further

review. (According to the Old Measures,

all CDM project companies applied

directly to the central NDRC for approval.)

The New Measure also changes the

sharing percentage in the proceeds

from the transfer of emission reductions

units between the government and

companies involved in N2O and PFC

projects.

• ThreeyearsCITexemptionisfollowedby

a 50 percent reduction for another three

years of the standard CIT rate for income

derived from qualified environmental

protection and energy or water

conservation projects. This reduction

starts from the year in which the first

revenue is generated. Applicable fields

include biomaterial energy, synergistic

development and utilization of methane,

and technological innovation in energy

conservation and emission.

• Tenpercentoftheamountinvestedinthe

qualified equipment is credited against

CIT payable for the current year, with

any unutilized investment credit eligible

to be carried forward for five tax years.

This applies only if such equipment is

qualified as special equipment related

to environmental protection, energy,

or water conservation and production

safety.

• Only90percentoftherevenuederived

from the transaction is taken into account

for CIT computation purposes. This

applies only if such revenue is derived

from the use of specific resources

associated with the synergistic utilization

of resources as raw materials in the

production of goods.

• A150percentdeductionisgivenfor

qualified R&D expenses incurred for CIT

computation purposes.

Value Added Tax (VAT)

• 50percentrefundofVATispaidonthe

sale of wind power.

• 100percentrefundofVATispaidonthe

sale of biodiesel oil generated by the

utilization of abandoned-animal fat and

vegetable oil.

• VATpaidonthesaleofgoodsproduced

from recycled materials or waste

residuals is refundable.

• VATisexemptonthesaleofself-

produced goods including recycled water,

qualified powdered rubber made out of

obsolete tires, retrodden tires and certain

construction materials made from 30

percent or more of waste residuals.

• VATisexemptforsewagetreatment,

garbage disposal and sludge treatment

services.

In November 2011, the government

authority expanded the scope of sales of

self-produced goods/products by using

the prescribed recycled materials, waste

residuals and agricultural residuals that are

eligibleforVATrefundatratesrangingfrom

50to100percentoftheVATpayable.The

rates may vary depending on the nature of

recycled materials or residuals utilized.

As of 1 April 2013, the taxpayer is further

required to meet the local/national pollutant

emission requirements in order to receive

theVATincentiveforself-producedgoods/

products from recycled materials.

Vehicle and Vessel Tax

As of 1 January 2012, qualified energy

efficient vehicles and vessels enjoy a 50

percentVehicleandVesselTaxdeduction.

Qualified new energy (mainly electric)

vehicles and vessels may be exempted

fromVehicleandVesselTaxes.

Financialsubsidiesandtaxincentives

available to energy performance

contracting(EPC)projects

• Financialsubsidiesaregrantedbythe

central and provincial government

agencies respectively. The standard rate

of subsidies at the central level is Chinese

yuan (CNY) 240 per ton of standard coal

saved. The standard rate at the provincial

level is no less than CNY60 per ton of

standard coal saved. The NDRC and

Ministry of Finance jointly announce

the qualified energy service companies

(ESCO). These companies can apply for

financial subsidies on energy preservation

management contracts. The list of

qualified ESCOs is updated on a regular

basis. These financial subsidies are rolled

out under the jurisdiction of Energy

Performance Contracting (EPC), and they

should be taxable for CIT purposes.

© 2013 KPMG International Cooperative (“KPMG International”). KPMG International provides no client services and is a Swiss entity with which the independent member firms of the KPMG network are affiliated.

17 | Taxes and incentives for renewable energy

• AqualiedESCOtakingpartinanEPC

project will be eligible for a tax exemption

in the first three years and a tax reduction

by half (an effective rate of 12.5 percent)

over the following three years, starting

from the tax year in which the revenue

from the project first arises.

• Anenterprisethatinvestsinspecial

equipment for energy conservation will

obtain a credit against its tax payable

that equals 10 percent of the investment

amount in the year in which the

investment is made. Where there is not

sufficient tax payable to absorb the credit

in the year, the excess credit may be

carried forward up to five tax years.

• AqualiedESCOtakingpartinanEPC